Introduction: The “Smart Investor” Trap

If you’re reading this, you check your Portfolio Analysis statement.

You notice when the market is up or down.

You notice that your portfolio is down, you are worried about no returns.

You might even compare your fund’s performance to a benchmark or a friend’s portfolio.

That makes you attentive.

It makes you proactive.

In the world of investing, it makes you smart.

But I need to tell you something important.

The very habit that makes you feel in control—constantly checking returns—might be the very thing keeping you anxious and stuck.

The entire financial industry is designed to keep you focused on one thing: performance. Past returns, star ratings, the “top 5 funds of the year.”

We’re taught that sophisticated Portfolio Analysis means diving deep into CAGR, alpha, and trailing returns.

This is what I call the “Returns-First” approach. It feels intelligent, but it’s backwards.

It puts the cart before the horse.

Why?

Because when you start by analysing returns, you’re judging your journey only by your current speed, with no map for your destination.

A fund might be speeding along beautifully, but if it’s on the wrong road for your goals, you’ll never arrive where you need to be.

At iNVESTT.in, we flip this script.

The first and most critical question in any Portfolio Analysis isn’t “How much did I make?”

It’s “Is my money where it needs to be?”

This post is your guide to a different kind of analysis.

It’s the difference between feeling confused by market noise and being in control of your financial future.

We’ll start by understanding the cycle that’s likely keeping you trapped.

Why Your Current “Portfolio Analysis” is Setting You Up to Fail

Let’s name the cycle you’re probably familiar with. I see it every day with investors who come to me for a review.

It works like this:

Market goes up → You check your portfolio value, see the green numbers, and feel a surge of confidence.

You might even think, “My advisor was right about that fund.”

Market goes down or sideways → You open your statement, see the red, and feel a knot in your stomach.

Questions flood in: “Should I switch funds?” “Is my advisor doing a bad job?” “Should I stop my SIP?”

This is the Returns-First Loop of Anxiety.

It’s a reactive, emotional rollercoaster.

And it’s exhausting.

But here’s the crucial insight: This cycle is completely disconnected from your life goals.

The performance of a small-cap fund this quarter has nothing to do with your child’s college fees due in 8 years.

The downturn in a flexi-cap fund tells you nothing about whether you’re on track for retirement in 15 years.

You’re trying to assess the health of your financial plan by listening to the daily weather report.

It’s all noise without the context of a specific goal and its time horizon.

This noise is overwhelming.

But more importantly, this loop keeps you reactive and anxious because it’s built on a shaky foundation: analysing returns without context.

To build something stable, you need a foundation entirely different.

That foundation is ‘goal-alignment’.

If analysing returns in isolation is the shaky foundation—the source of the noise and anxiety—then measuring ‘goal-alignment’ is the solid ground you can build upon.

This is the non-negotiable first step in any intelligent portfolio analysis.

Let me show you what this means with a practical example.

It’s a shift from watching the speedometer to consulting the map.

The iNVESTT.in Flip: Goal-Alignment as the First Metric

Imagine an investor—let’s call him Rohan.

He’s 40, has been investing for years, and has a portfolio worth about ₹50 lakhs spread across 8 different funds.

When he looks at his consolidated statement, the overall returns look “decent.”

His advisor tells him to stay the course.

But when we sit down, we ignore the return numbers completely at first.

Instead, we do a Goal-Alignment Audit.

We ask: “What is each rupee in this portfolio meant to achieve?”

We start by listing his clear financial goals:

- Child’s University Fund: ₹30 lakhs needed in 8 years.

- House Down Payment: ₹20 lakhs needed in 3 years.

Next, we apply a fundamental rule of investing: the time horizon dictates the asset class.

- A goal 8+ years away can use growth engines (Equity).

- A goal needed in just 3 years requires stability (Debt or Conservative Hybrid).

Now, we audit his portfolio.

The critical question is not “Is this a good fund?”

But “Is this fund in the right category for the goal it’s serving?”

Here’s a simplified view of what that analysis looks like:

| Goal | Time Left | Correct Fund Category | Fund Rohan Actually Holds | Alignment? |

| Child’s University (₹30L) | 8 years | Equity (Large & Mid Cap) | A Flexi Cap Fund | Yes |

| House Down Payment (₹20L) | 3 years | Debt / Hybrid | A Large Cap Fund | No – Red Flag |

See the problem? It’s glaring.

For his down payment goal, Rohan is taking a massive, unnecessary risk.

A Large -cap fund is designed for 5+ year horizons.

Over 3 years, it could easily be down – 20% just when he needs the money.

The fund’s past returns are irrelevant; the category mismatch is the real danger.

This “Alignment Check” is the single most important part of portfolio analysis.

It reveals a structural risk that no return number can show.

It tells you if you’re in the right vehicle for the journey, regardless of how fast it’s currently moving.

This check strips away the complexity and emotion.

You’re no longer a passenger worrying about speed bumps; you become the navigator, ensuring every part of the engine is geared for its specific route.

And once you see a mismatch, it becomes your absolute priority to fix.

Returns are a secondary discussion until this structural integrity is in place.

So, how do you perform this alignment check on your own portfolio?

The process is straightforward.

It requires clarity, not complexity.

You can break the Returns-First Loop yourself by following these four steps.

Think of it as a personal portfolio health check-up.

Your Action Plan: From Confusion to Clarity in 4 Steps

Step 1: List Your Goals & Timelines – Get Specific

This is where most investors stall.

“Wealth creation” or “a good retirement” are not goals; they are wishes.

A goal has a name, a cost, and a deadline.

Instead of: “Save for child’s education.”

Write: “₹30 lakhs for Ananya’s engineering degree, needed in July 2032.” (That’s 8 years from now).

The easiest way to do this is to stop guessing and use a structured tool.

Our free Goal Planner is designed specifically for this first, critical step.

It helps you move from vague dreams to clear, actionable targets.

Spend 10 minutes here—it forms the bedrock of everything that follows.

Step 2: Map Each Goal to a ‘Correct’ Fund Category

Use a simple, rule-based framework. Your goal’s time horizon is the primary dictator.

< 3 years: Park it. Use Debt Funds, Arbitrage Funds, or simply a high-yield savings account. Capital preservation is key.

3 to 7 years: This is the middle ground. Consider Conservative Hybrid Funds or Balanced Advantage Funds. You need some growth, but cannot afford high equity volatility.

7+ years: This is the domain of Equity Funds (Large Cap, Flexi Cap, Mid Cap, etc.).

Time is your ally to weather market cycles.

This mapping isn’t about picking winners; it’s about assigning the right type of vehicle for each journey.

Step 3: The Audit – The Moment of Truth

Take your current portfolio statement. For each investment (SIP or lump sum), ask yourself: “Which goal is this money serving?”

Then, check the fund’s category against the “Correct Category” from Step 2.

Is the SIP for your 5-year car purchase going into a mid-cap fund? Mismatch.

Is your 10-year+ retirement corpus sitting largely in debt funds? Mismatch.

Create your own simple table, just like Rohan’s. The column “Alignment? (Yes/No)” will give you your diagnosis.

Step 4: Interpret & Prioritise

If all ‘Yes’: Congratulations.

Your portfolio has structural integrity.

Now you can proceed to the secondary analysis to determine which equity or debt funds are the best within their respective categories.

If you see ‘No’: This is your number one financial priority.

Do not get distracted by market news or fund performance.

A category mismatch is a fundamental risk that must be corrected.

This usually means a strategic reallocation—shifting money from the wrong category to the right one.

This process removes emotion.

You’re no longer reacting to the market’s mood; you’re executing a plan based on your life’s blueprint.

The anxiety of the “Returns-First Loop” fades because you have a clear rationale for every investment you hold.

But this leads to a fair question.

Once the structure is sound, then do we look at returns?

Absolutely, we do.

But with a crucial shift in perspective.

Returns are not the starting point for selection; they are the final checkpoint for efficiency.

Once your portfolio is structurally sound—meaning every rupee is in the correct asset category for its goal—then your analysis can ask: “Within this category, am I in the best possible fund?”

This is where smart analysis moves from checking the map to fine-tuning the engine.

What About Returns? Their Rightful (Second) Place

Forget chasing the “top performer” of last year.

That’s a loser’s game.

Instead, we look for probability and consistency.

We want funds that have a high likelihood of doing their job well over the full market cycle.

How do we measure this?

We use data to assess behaviour, not just outcomes.

Let’s take a real-world example.

Suppose your goal-alignment check confirms you need a Flexi Cap fund for a long-term goal.

You’ve shortlisted two major funds: Parag Parikh Flexi Cap Fund and HDFC Flexi Cap Fund. On the surface, their 5-year average returns might look similar.

But the real story is in their consistency.

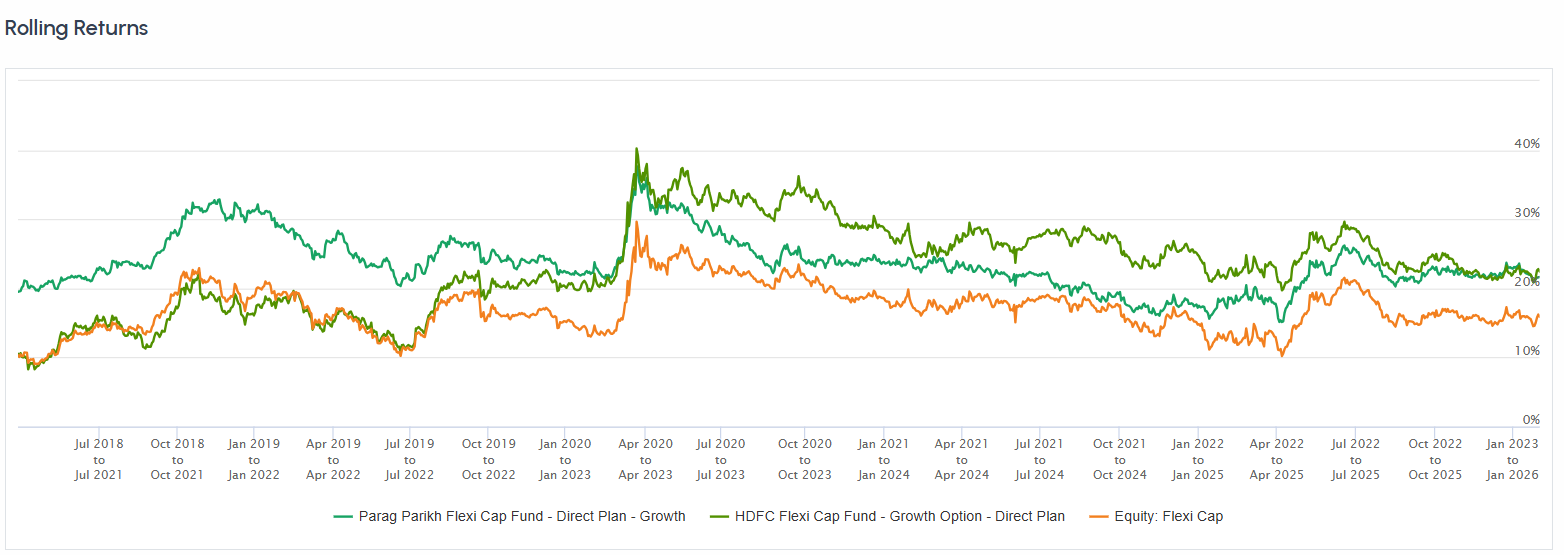

We used our Rolling Returns Calculator to analyse every possible 3-year investment period

from April 2018 to today—a timeframe that includes a bull run, a crash, and a recovery.

Here’s what the data tells us:

| Key Metric | Parag Parikh Flexi Cap | HDFC Flexi Cap | What it means for you |

| Average 3-Year Return | 23.63% | 23.03% | Superficially, they are nearly identical. |

| Minimum 3-Year Return | 15.13% | 8.28% | Critical Difference. In its worst 3-year period, Parag Parikh still delivered 15%.

HDFC’s worst was 8.3%. This is downside protection. |

| % of times return >20% | 85.2% | 70.9% | Consistency. Parag Parikh delivered >20% returns in 85% of all 3-year periods. HDFC did so 71% of the time. |

| % of times return 12-20% | 14.8% | 24.7% | HDFC had more periods of “good but not great” returns. |

The conclusion is clear.

While both funds have delivered similar average returns over the last 8 years, Parag Parikh Flexi Cap has demonstrated far greater consistency and downside resilience.

For you, the investor, this translates to a higher probability and lower anxiety.

You’re not just hoping for a good average; you’re choosing a fund whose worst-case scenario over any 3 years was a solid 15% return.

This is the essence of structural strength.

This method—judging a fund by the distribution of its outcomes over time—is probability-based selection.

We’re not predicting the future; we’re identifying funds whose past behavior gives us statistical confidence in their structure and process.

It’s why, at iNVESTT.in, we priorities rolling returns and consistency checks over trailing returns or star ratings.

Star ratings often miss this nuance, which is why they are a poor tool for final selection.

Conclusion: Becoming a Truly Smart Investor

Let’s recap the smart investor’s portfolio analysis:

Start with Goals: Define them with names, costs, and deadlines. Use the free Goal Planner to make this simple.

Check Alignment: Conduct your Goal-Alignment Audit. This is your non-negotiable first step—fix any category mismatches before you look at returns.

Then, Check Quality: Within the correct category, use tools like the Rolling Returns Calculator to select funds based on probability and consistency, not just past performance.

This framework is your filter. It turns down the market noise.

The next time you feel that familiar anxiety to check your portfolio’s value, pause.

Run the Alignment Check instead.

You’ll immediately know if your concern is just short-term noise or a genuine structural problem that needs your attention.

From Foundation to Mastery

What we’ve covered here is the essential foundation—the mindset and first steps to move from being market-dependent to goal-driven.

It’s what stops you from making costly emotional mistakes.

Your immediate next step is to put this into practice.

Use our free Goal Planner to translate your goals from vague ideas into clear, actionable targets.

This clarity alone will change how you view your portfolio.

If you want a professional, data-driven diagnosis of your existing portfolio—to see exactly where your goal-alignments and category mismatches are—consider booking a Portfolio Review Consultation.

As a SEBI Registered Research Analyst, I use our algorithm to give you a clear, actionable roadmap.

Once your goals are crystal clear, the next level of mastery involves the specific metrics for probability-based selection, knowing exactly when to sell a fund, and constructing a compact portfolio.

That deeper, integrated system—including the ‘Golden Triangle Method’—is what I’ve compiled for serious investors in my guide, “7 Insider Secrets to Select a Winning Mutual Fund.”

Final Thought

Your portfolio is not a collection of tickers and return percentages.

It is the engine for your life’s goals.

Build it with the right foundation, fuel it with a smart, repeatable process, and you won’t just be a smart investor—you’ll be a confident and successful one.