Introduction

How to choose mutual funds is a question every investor asks. But most start at the wrong place.

“Which fund gave the highest return?” That is the first question most investors ask. It is also the wrong question.

You have seen this play out. You pick a fund because its returns look amazing. A year later, it is struggling. You feel cheated. You wonder what you missed.

Here is what you missed. Returns alone hide everything that matters. Consistency. Benchmark performance. Downside behavior.

Let us show you what to look at instead.

The Return Trap

Here is how most investors choose funds. Open a website. Sort by returns. Pick the fund with the biggest number. Done.

This feels logical. Higher returns mean more money. Why would you not pick the highest?

Because that number does not tell you how the fund got there.

A fund can have a great 5-year return because of one exceptional year. The other four years it may have underperformed. You would never know by looking at the final number.

Another fund might have a slightly lower 5-year return but beat its benchmark year after year. Steady. Reliable. Boring.

Which one would you rather hold for 10 years?

The first fund tricks you with a flashy number. The second fund builds wealth quietly.

Returns alone cannot tell you the difference. Stop Chasing Last Year’s Top Mutual Funds.

So what should you look at instead? Let us get to the data.

What The Data Shows

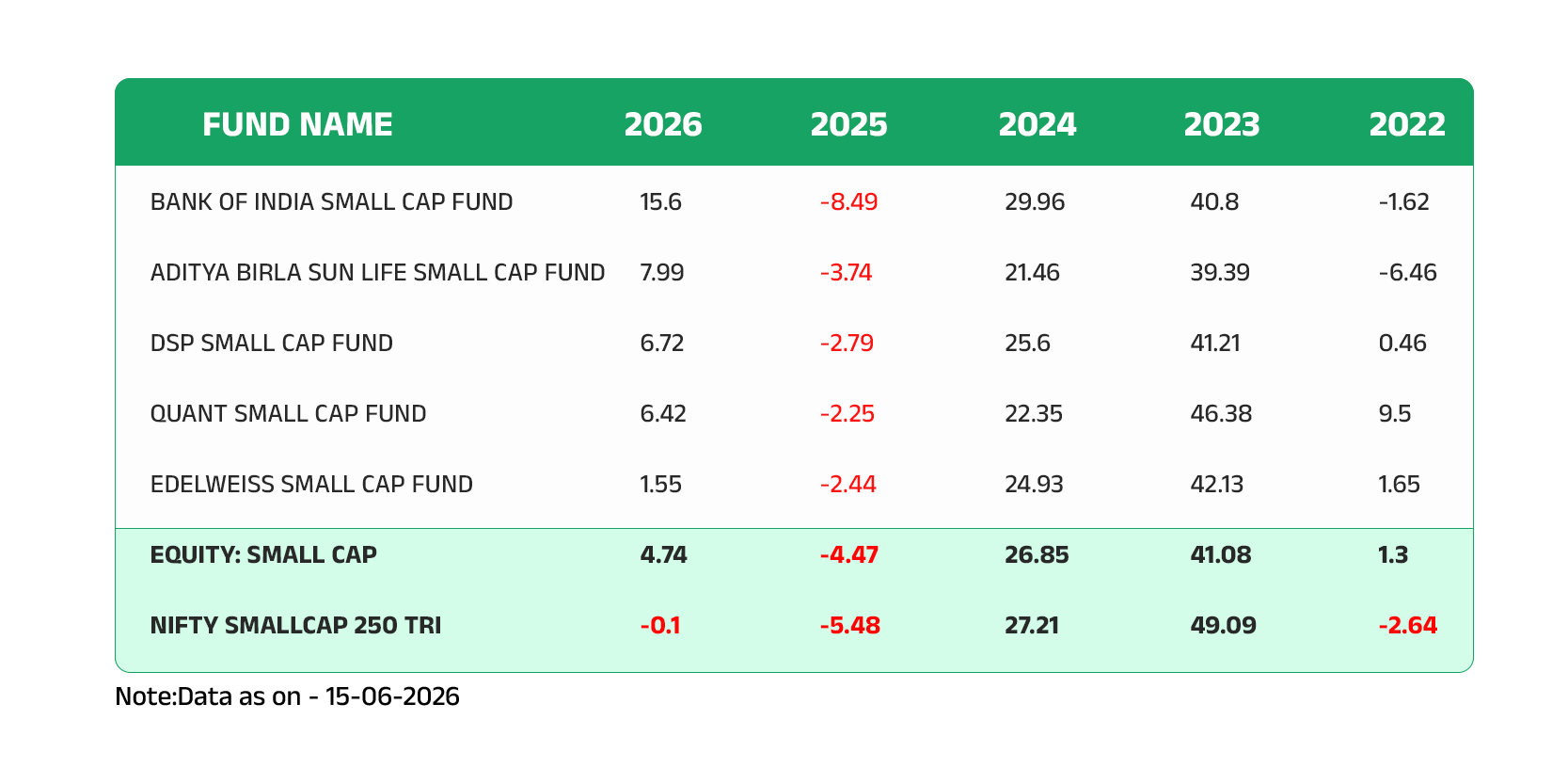

Let us look at five Small Cap funds over five years. The table below shows their yearly returns from 2022 to 2026.

The bottom row is the benchmark. The index these funds are trying to beat.

Now look closely. In 2023, the benchmark returned 49.09%. Almost every fund fell short of that except Quant at 46.38%. But that is not the full story.

Look at 2025. The benchmark fell -5.48%. DSP fell only -2.79%. Quant fell -2.25%. Both protected better than the index. Bank of India fell harder at -8.49%.

Now look at 2022. Benchmark fell -2.64%. Quant actually delivered +9.5%. DSP and Edelweiss also stayed positive.

Here is a better question than “which fund had the highest return?” How many years did each fund beat the benchmark?

Bank of India beat the benchmark in four out of five years. Aditya Birla beat it only twice. The other three funds beat it three times each.

Notice something. The fund with the flashiest single year is not the most consistent. And the most consistent fund did not have the highest 5-year number.

This is what matters more than returns. Consistency against the benchmark.

But there is more. How a fund behaves when the market falls tells you even more about its quality.

What Matters More Than Returns

Let us go back to the table. Three things stand out more than absolute returns.

First, consistency against benchmark.

Bank of India beat the benchmark in four out of five years. That means in most market conditions, it did its job.

Aditya Birla beat it only twice. That means in three out of five years, it failed to deliver what an index fund would have given you for free.

Which fund would you trust for the next ten years? The one that does its job most years, or the one that fails more often than it succeeds?

Second, downside behavior.

Look at 2025, a down year. The benchmark fell -5.48%. DSP fell only -2.79%. Quant fell -2.25%. Both protected your capital better than the market.

Now look at Bank of India in the same year. It fell -8.49%. Worse than the benchmark.

A fund that loses less in bad years helps you stay invested. You panic less. You sell less. You stay for the recovery.

Third, risk-adjusted behavior.

Returns do not tell you how bumpy the ride was.

Two funds with the same 5-year return can feel completely different.

One is smooth. The other is a roller coaster.

Sharpe Ratio and Alpha help measure this.

So when you choose a fund, stop starting with returns. Start with these three questions.

How To Choose A Mutual Fund

Stop asking “Which fund gave the highest return?”

Start asking these three questions instead.

One. How often does this fund beat its benchmark?

Look at +5 years of yearly data. Count the number of years the fund beat its index. If it beats the benchmark in 4 out of 5 years, that is a good sign. If it beats it only 2 times, that fund is failing more often than it succeeds.

Two. How does it behave in down years?

Find the years when the benchmark fell. Did the fund fall less? Did it stay positive? A fund that protects capital in bad years is worth more than a fund that skyrockets in good years and crashes in bad ones.

Three. Is the consistency there across 5+ years?

One good year is luck. Three good years in a row is a pattern. Five years or more of consistent benchmark-beating performance is evidence.

If a fund beats its benchmark in most years and protects well in down years, it is a good fund. Even if its 5-year return is not the highest number on the screen.

The highest number often disappoints. The steady performer quietly builds wealth.

Now you know what to look for. But how do you actually compare two funds side by side?

Conclusion

Let us go back to where we started.

How to choose mutual funds is a question every investor asks. But most start at the wrong place. They chase the highest number, as we explained in Stop Chasing Last Year’s Top Mutual Funds.

Then they wonder why their fund struggles the next year. That happens because top performers rarely stay on top, something we covered in Why Top-Performing Funds Change Every Year.

Returns are not useless. They are just not where you should start.

Start with consistency against the benchmark. Look at how the fund behaves in down years. Check if the performance holds up across five years or more.

A fund that beats its benchmark in four out of five years and protects your capital in bad years is a good fund. Even if its five-year number is not the flashiest.

The highest number often disappoints. The steady performer quietly builds wealth.

If you are holding a fund and wondering whether it is genuinely good or just had one lucky year, book a call with us. We will review your portfolio together.

Disclaimer:

This article is for educational and informational purposes only and should not be construed as investment advice, investment recommendation, or solicitation to buy, sell, or hold any securities.

The views and opinions expressed are based on information believed to be reliable as on the date of publication. However, no representation or warranty is made regarding the accuracy, completeness, or adequacy of the information.

Investments in securities are subject to market risks. Readers should conduct their own research and consult their financial adviser before making any investment decisions.

SEBI Registration No.: INH000010858

Analyst Name: Gopi krishna Matcha

Pingback: Common Mutual Fund Comparison Mistakes (And How to Avoid Them)